This year's edition has a special purpose. It is designed to inform the energy and climate debates at the UNFCCC Conference of the Parties (COP26) in November 2021 and beyond. As such, it departs from the usual WEO structure in the way it organises and presents the material and analyses.

This is the executive summary of the report

Click here to download the full report

A new global energy economy is emerging…

In 2020, even while economies bent under the weight of Covid-19 lockdowns, renewable sources of energy such as wind and solar PV continued to grow rapidly, and electric vehicles set new sales records. The new energy economy will be more electrified, efficient, interconnected, and clean. Its emergence is the product of a virtuous circle of policy action and technology innovation, and its momentum is now sustained by lower costs. In most markets, solar PV or wind now represents the cheapest available source of new electricity generation. Clean energy technology is becoming a major new area for investment and employment – and a dynamic arena for international collaboration and competition.

…but the transformation still has a long way to go

At the moment, however, every data point showing the speed of change in energy can be countered by another showing the stubbornness of the status quo. The rapid but uneven economic recovery from last year’s Covid-induced recession is putting major strains on parts of today’s energy system, sparking sharp price rises in natural gas, coal, and electricity markets.

For all the advances being made by renewables and electric mobility, 2021 is seeing a large rebound in coal and oil use. Largely for this reason, it is also seeing the second-largest annual increase in CO2 emissions in history. Public spending on sustainable energy in economic recovery packages has only mobilised around one-third of the investment required to jolt the energy system onto a new set of rails, with the largest shortfall in developing economies which continue to face a pressing public health crisis.

Progress towards universal energy access has stalled, especially in sub-Saharan Africa. The direction of travel is a long way from alignment with the IEA’s landmark Net Zero Emissions by 2050 Scenario (NZE), published in May 2021, which charts a narrow but achievable roadmap to a 1,5°C stabilisation in rising global temperatures and the achievement of other energy-related sustainable development goals.

At a pivotal moment for energy and climate, the WEO-2021 provides an essential guidebook for COP26 and beyond

Pressures on the energy system will not relent in the coming decades. The energy sector is responsible for almost three-quarters of the emissions which have already pushed global average temperatures 1,1°C higher since the pre-industrial age, with visible impacts on weather and climate extremes. The energy sector has to be at the heart of the solution to climate change.

At the same time, modern energy is inseparable from the livelihoods and aspirations of a global population that is set to grow by some 2-billion people to 2050, with rising incomes pushing up demand for energy services, and many developing economies navigating what has historically been an energy- and emissions-intensive period of urbanisation and industrialisation. Today’s energy system is not capable of meeting these challenges; a low emissions revolution is long overdue.

This special edition of the World Energy Outlook (WEO) has been designed to assist decision makers at the 26th Conference of the Parties (COP26) and beyond by describing the key decision points which could move the energy sector onto safer ground. It provides a detailed stocktake of how far countries have come in their clean energy transitions, how far they still have to go to reach the 1,5°C goal, and the actions that governments and others can take to seize opportunities and avoid pitfalls along the way. With multiple scenarios and case studies, this WEO explains what is at stake, at a time when informed debate on energy and climate is more important than ever.

Announced climate pledges move the needle…

In the run-up to COP26, many countries have put new commitments on the table, detailing their contributions to the global effort to reach climate goals; more than 50 countries, as well as the entire European Union, have pledged to meet net zero emissions targets. If these are implemented in time and in full, as modelled in detail in our new Announced Pledges Scenario (APS), they start to bend the global emissions curve down.

Over the period to 2030, low emissions sources of power generation account for the vast majority of capacity additions in this scenario, with annual additions of solar PV and wind approaching 500 GW by 2030. As a result, coal consumption in the power sector in 2030 is 20% below recent highs. Rapid growth in electric vehicle sales and continued improvements in fuel efficiency will lead to a peak in oil demand around 2025.

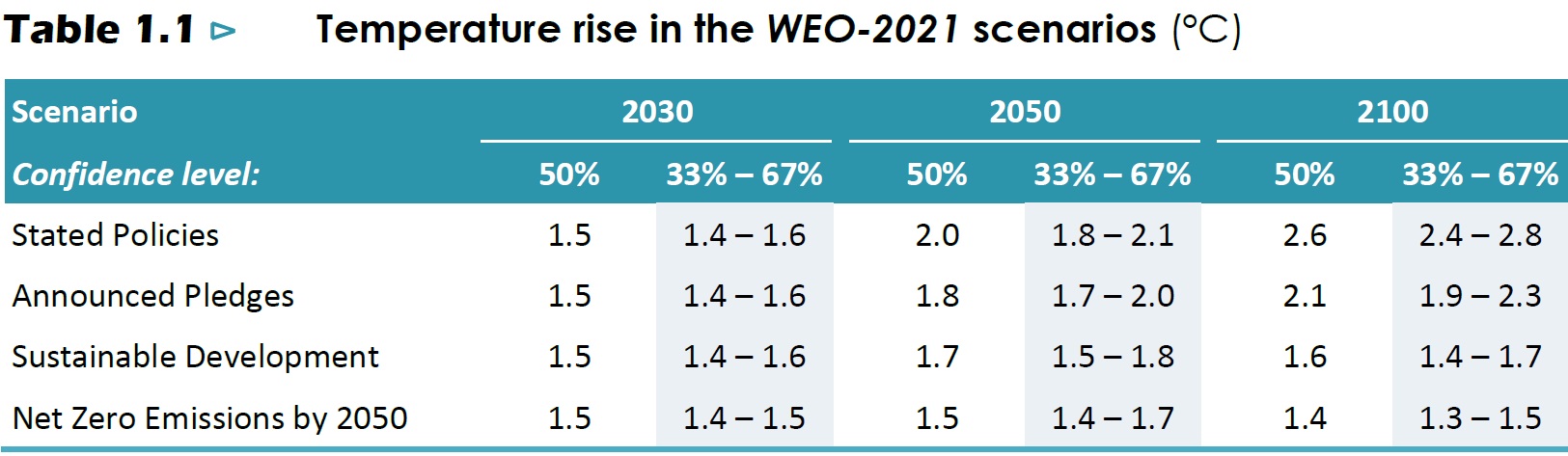

Efficiency gains mean that global energy demand plateaus post-2030. The successful pursuit of all announced pledges means that global energy-related CO2 emissions fall by 40% over the period to 2050. All sectors see a decline, with the electricity sector delivering by far the largest. The global average temperature rise in 2100 is held to around 2,1°C above pre-industrial levels, although this scenario does not hit net zero emissions, so the temperature trend has still not stabilised.

…but achieving these pledges in full and on time cannot be taken for granted

A lot more needs to be done by governments to fully deliver on their announced pledges. Looking sector-by-sector at what measures governments have actually put in place, as well as specific policy initiatives that are under development, reveals a different picture, which is depicted in our Stated Policies Scenario (STEPS).

This scenario also sees an accelerating pace of change in the power sector, sufficient to realise a gradual decline in the sector’s emissions even as global electricity demand nearly doubles to 2050. However, this is offset by continued growth in emissions from industry, such as the production of cement and steel, and heavy-duty transport, such as freight trucks. This growth largely comes from emerging market and developing economies as they build up their nationwide infrastructure.

In the STEPS, almost all of the net growth in energy demand to 2050 is met by low emissions sources, but that leaves annual emissions at around current levels. As a result, global average temperatures are still rising when they hit 2,6°C above pre-industrial levels in 2100.

Today’s pledges cover less than 20% of the gap in emissions reductions that needs to be closed by 2030 to keep a 1,5°C path within reach

The APS sees a doubling of clean energy investment and financing over the next decade, but this acceleration is not sufficient to overcome the inertia of today’s energy system.

In particular, over the crucial period to 2030, the actions in this scenario fall well short of the emissions reductions that would be required to keep the door open to a Net Zero Emissions by 2050 trajectory. One of the key reasons for this shortfall is that today’s climate commitments, as reflected in the APS, reveal sharp divergences between countries in the pledged speeds of their energy transitions.

Alongside its achievements, this scenario also contains the seeds of new divisions and tensions, in the areas of trade in energy-intensive goods, for example, or in international investment and finance. Successful, orderly, and broad-based energy transitions depend on finding ways to lessen the tensions in the international system that are highlighted in the APS. All countries will need to do more to align and strengthen their 2030 goals and make this a collaborative global transition in which no one is left behind.

Solutions to close the gap with a 1,5°C path are available – and many are highly cost-effective

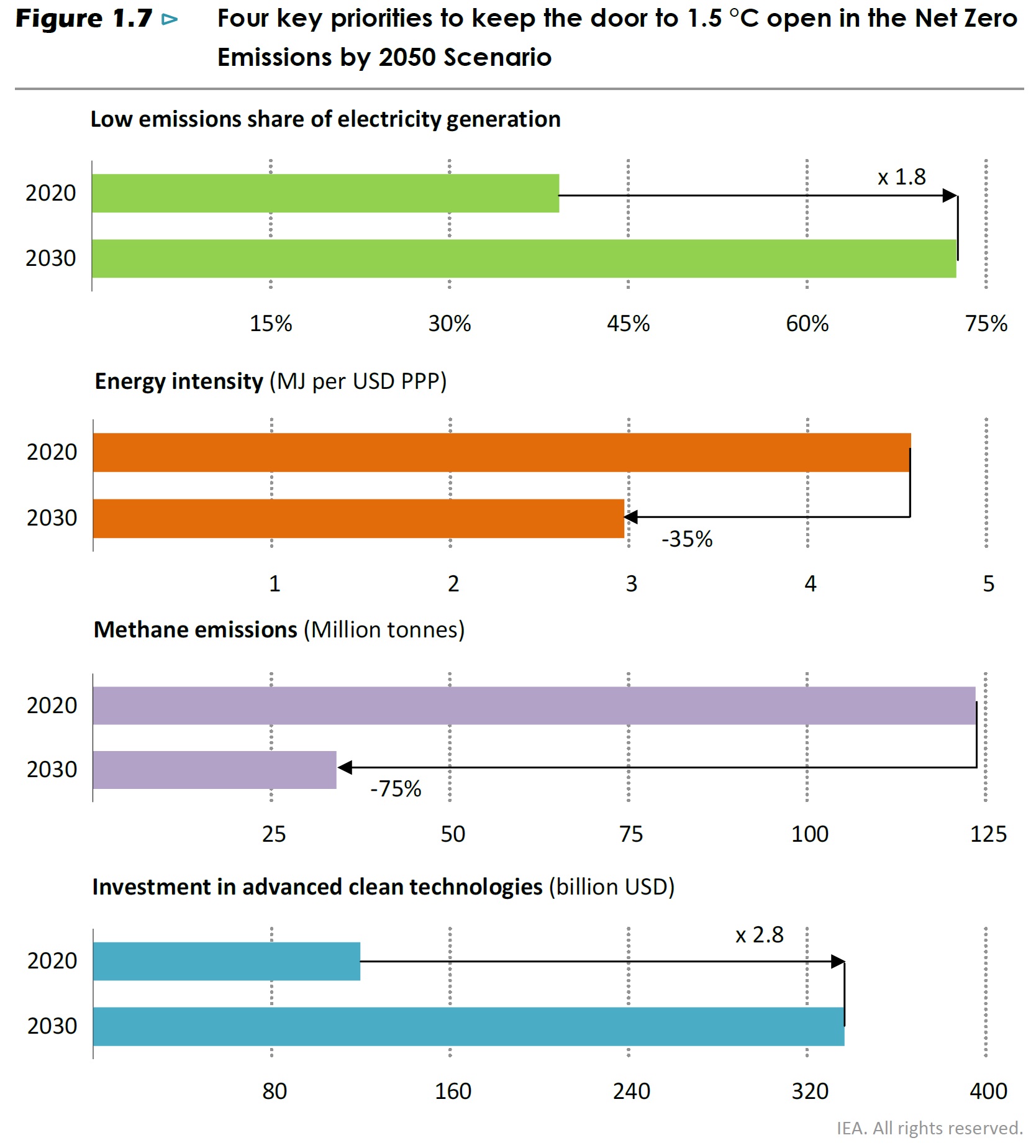

The WEO-2021 highlights four key measures that can help to close the gap between today’s pledges and a 1,5°C trajectory over the next ten years – and to underpin further emissions reductions post-2030 (see Figure 1.7). More than 40% of the actions required are cost-effective, meaning that they result in overall cost savings to consumers compared with the pathway in the APS.+

All countries need to do more: those with existing net zero pledges account for about half of the additional reductions, notably China.

The four measures are:

- A massive additional push for clean electrification that requires a doubling of solar PV and wind deployment relative to the APS; a major expansion of other low-emissions generation, including the use of nuclear power where acceptable; a huge build-out of electricity infrastructure and all forms of system flexibility, including from hydropower; a rapid phase out of coal; and a drive to expand electricity use for transport and heating. Accelerating the decarbonisation of the electricity mix is the single most important lever available to policy makers: it closes more than one-third of the emissions gap between the APS and NZE. With improved power market designs and other enabling conditions, the low costs of wind and solar PV mean that more than half of the additional emissions reductions could be gained at no cost to electricity consumers.

- A relentless focus on energy efficiency, together with measures to temper energy service demand through materials efficiency and behavioural change. The energy intensity of the global economy decreases by more than 4% per year between 2020 and 2030 in the NZE – more than double the average rate of the previous decade. Without this improvement in energy intensity, total final energy consumption in the NZE would be about one-third higher in 2030, significantly increasing the cost and difficulty of decarbonising energy supply. We estimate that almost 80% of the additional energy efficiency gains in the NZE over the next decade result in cost savings to consumers.

- A broad drive to cut methane emissions from fossil fuel operations. Rapid reductions in methane emissions are a key tool to limit near-term global warming, and the most cost-effective abatement opportunities are in the energy sector, particularly in oil and gas operations. Methane abatement is not addressed quickly or effectively enough by simply reducing fossil fuel use; concerted efforts from governments and industry are vital to secure the emissions cuts that close nearly 15% of the gap to the NZE.

- A big boost to clean energy innovation. This is another crucial gap to be filled in the 2020s, even though most of the impacts on emissions are not felt until later. All the technologies needed to achieve deep emissions cuts to 2030 are available. But almost half of the emissions reductions achieved in the NZE in 2050 come from technologies that today are at the demonstration or prototype stage. These are particularly important to address emissions from iron and steel, cement, and other energy-intensive industrial sectors – and also from long-distance transport. Today’s announced pledges fall short of key NZE milestones for the deployment of hydrogen-based and other low-carbon fuels, as well as carbon capture, utilisation and storage (CCUS).

Finance is the missing link to accelerate clean energy deployment in developing economies

Getting the world on track for 1,5°C requires a surge in annual investment in clean energy projects and infrastructure to nearly US$4 trillion by 2030. Some 70% of the additional spending required to close the gap between the APS and NZE is needed in emerging market and developing economies. There have been some notable examples of developing economies mobilising capital for clean energy projects, such as India’s success in financing a rapid expansion of solar PV in pursuit of its 450 GW target for renewables by 2030.

However, there have also been persistent challenges, many of which have been exacerbated by the pandemic. Funds to support sustainable economic recovery are scarce and capital remains up to seven-times more expensive than in advanced economies. In some of the poorest countries in the world, Covid-19 also broke the trend of steady progress towards universal access to electricity and clean cooking. The number of people without access to electricity is set to rise by 2% in 2021, with almost all of the increase in sub-Saharan Africa.

An international catalyst is essential to accelerate flows of capital in support of energy transitions and allow developing economies to chart a new lower emissions path for development. Most transition-related energy investment will need to be carried out by private developers, consumers and financiers responding to market signals and policies set by governments. Alongside the necessary policy and regulatory reforms, public financial institutions – led by international development banks and larger climate finance commitments from advanced economies – play crucial roles to bring forward investment in areas where private players do not yet see the right balance of risk and reward.

Strategies to phase out coal have to effectively deal with impacts on jobs and electricity security

Coal demand declines in all our scenarios, but the difference between the 10% decline to 2030 in APS and the 55% decline in NZE is the speed at which coal is phased out from the power sector.

This has four components:

- Halting the approval of new, unabated coal plants

- Reducing emissions from the 2100 GW of operating plants, which produced more than one-third of the world’s electricity in 2020

- Investing – at sufficient scale – to reliably meet the demand that would otherwise have been met by coal; and

- Managing the economic and social consequences of change.

Approvals of new coal-fired plants have slowed dramatically in recent years, stemmed by lower cost renewable energy alternatives, rising awareness of environmental risks, and increasingly scarce options for financing. Yet some 140 GW of new coal plants are currently under construction and more than 400 GW are at various stages of planning.

China’s announcement of an end to support for building coal plants abroad is potentially very significant: it could lead to the cancellation of up to 190 GW of coal projects that are built in the APS. This could save some 20 Gt in cumulative CO2 emissions if these plants are replaced with low emissions generation – an amount comparable to the total emissions savings from the European Union going to net zero by 2050.

Bringing down emissions from the existing global coal fleet requires a broad-based and dedicated policy effort. In our scenarios, coal plants are either retrofitted with CCUS, reconfigured to be co-fired with low emissions fuels such as biomass or ammonia, repurposed to focus on system adequacy, or retired. Retirements in the APS occur at twice the rate seen in the last decade, and the rate nearly doubles again in the NZE to reach almost 100 GW of retirements per year. Policy interventions need to focus on retiring plants that would not otherwise have done so while also supporting measures to bring down emissions from the remaining fleet. Support must be there for those who lose jobs in declining sectors.

Managing the phaseout of coal depends on early and sustained engagement by governments and financial institutions to mitigate the impacts on affected workers and communities, and to allow for the reclamation and repurposing of lands. Energy transitions create dislocations: many more new jobs are created, but not necessarily in the same places where jobs are lost. Skill sets are not automatically transferable, and new skills are needed. This is true both within specific countries and internationally. Governments need to manage the impacts carefully, seeking transition pathways that maximise opportunities for decent, high-quality work and for workers to make use of their existing skills – and mobilising long-term support for affected workers and communities.

Liquids and gases are caught between scenarios

Oil demand, for the first time, goes into eventual decline in all the scenarios examined in the WEO-2021, although the timing and speed of the drop vary widely. In the STEPS, the high point in demand is reached in the mid-2030s and the decline is very gradual. In the APS, a peak soon after 2025 is followed by a decline towards 75 million barrels per day (mb/d) by 2050. To meet the requirements of the NZE, oil use plummets to 25 mb/d by mid-century.

Natural gas demand increases in all scenarios over the next five years, but there are sharp divergences after this. Many factors affect to what extent, and for how long, natural gas retains a place in various sectors as clean energy transitions accelerate. The outlook is far from uniform across different countries and regions. In the NZE, a rapid rise in low emissions fuels is one of the key reasons – alongside greater efficiency and electrification – why no new oil and gas fields are required beyond those already approved for development.

Actual deployment of low emissions fuels is well off track. For example, despite the burgeoning interest in low-carbon hydrogen, the pipeline of planned hydrogen projects falls short of the levels of use in 2030 implied by announced pledges, and even further short of the amounts required in the NZE (which are nine-times higher than in the APS).

There is a looming risk of more turbulence ahead for energy markets

The world is not investing enough to meet its future energy needs, and uncertainties over policies and demand trajectories create a strong risk of a volatile period ahead for energy markets. Transition-related spending is gradually picking up but remains far short of what is required to meet rising demand for energy services in a sustainable way.

The deficit is visible across all sectors and regions. At the same time, the amount being spent on oil and natural gas, dragged down by two price collapses in 2014/15 and in 2020, is geared towards a world of stagnant or even falling demand for these fuels. Oil and gas spending today is one of the very few areas that it is reasonably well aligned with the levels seen in the NZE to 2030.

IEA analysis has repeatedly highlighted that a surge in spending to boost deployment of clean energy technologies and infrastructure provides the way out of this impasse, but this needs to happen quickly, or global energy markets will face a turbulent and volatile period ahead. Clear signals and direction from policy makers are essential. If the road ahead is paved only with good intentions, then it will be a bumpy ride indeed.

Transitions can offer some shelter for consumers against oil and gas price shocks

Energy transitions can provide a cushion from the shock of commodity price spikes if consumers can get help to manage the upfront costs of change. In a transforming energy system such as the NZE, households are less reliant on oil and gas to meet their energy needs, thanks to efficiency improvements, a switch to electricity for mobility, and a move away from fossil fuel-fired boilers for heating. For these reasons, a large commodity price shock in 2030 is 30% less costly to households in the NZE compared with in the STEPS. Reaching this point will require policies that assist households with the additional upfront costs of efficiency improvements and low emissions equipment such as electric vehicles and heat pumps.

As electricity takes up a progressively larger share of household energy bills, governments have to ensure that electricity markets are resilient by incentivising investments in flexibility, energy efficiency, and demand-side response.

Across all scenarios, the share of variable renewables in electricity generation expands to reach 40 to 70% by 2050 (and even higher in some regions), compared with an average of just under 10% today. In the NZE, there are some 240 million rooftop solar PV systems and 1,6 billion electric cars by 2050. Such a system will need to operate very flexibly, enabled by adequate capacity, robust grids, battery storage and dispatchable low emissions sources of electricity (like hydropower, geothermal and bioenergy, as well as hydrogen and ammonia-fired plants, or small modular nuclear reactors). This kind of system will also require digital technologies that can support demand side response and securely manage multi-directional flows of data and energy.

Other potential energy security vulnerabilities require close vigilance

Trade patterns, producer policies and geopolitical considerations remain critically important for energy security, even as the world shifts to an electrified, renewables-rich energy system. This relates in part to the way that energy transitions affect oil and gas as supplies become more concentrated in a smaller group of resource-rich countries – even as their economies simultaneously come under strain from lower export revenues.

Higher or more volatile prices for critical minerals such as lithium, cobalt, nickel, copper and rare earth elements could slow global progress towards a clean energy future or make it more costly. Price rallies for key minerals in 2021 could increase the costs of solar modules, wind turbines, electric vehicle (EV) batteries and power lines by 5 to 15%. If maintained over the period to 2030 in the NZE, this would add US$700 billion to the investment required for these technologies. Critical minerals, together with hydrogen-rich fuels such as ammonia, also become major elements in international energy-related trade; their combined share rises from 13% today to 25% in the APS and to over 80% in the NZE by 2050.

The costs of inaction on climate are immense, and the energy sector is at risk

Extreme weather events over the past year have highlighted the risks of unchecked climate change, and the energy sector will feel the impacts. Today, the world’s energy infrastructure is already facing increasing physical risks related to climate change, which emphasizes the urgent need to enhance the resilience of energy systems. We estimate that around one quarter of global electricity networks currently face a high risk of destructive cyclone winds, while over 10% of dispatchable generation fleets and coastal refineries are prone to severe coastal flooding, and one-third of freshwater-cooled thermal power plants are located in areas of high-water stress.

In the STEPS, the frequency of extreme heat events would double by 2050 compared with today – and they would be around 120% more intense, affecting the performance of grids and thermal plants while pushing up demand for cooling. A failure to accelerate clean energy transitions would continue to leave people exposed to air pollution. Today, 90% of the world’s population breathes polluted air, leading to over five million premature deaths a year. The STEPS sees rising numbers of premature deaths from air pollution during the next decade. In the NZE, there are 2,2 million fewer premature deaths per year by 2030, a 40% reduction from today.

The potential prize is huge for those who make the leap to the new energy economy

In the NZE, there is an annual market opportunity that rises well above US$1 trillion by 2050 for manufacturers of wind turbines, solar panels, lithium-ion batteries, electrolysers and fuel cells. This is comparable in size to the current global oil market.

This creates enormous prospects for companies that are well positioned along an expanding set of global supply chains. Even in a much more electrified energy system, there are major openings for fuel suppliers: companies producing and delivering low-carbon gases in 2050 are handling the equivalent of almost half of today’s global natural gas market.

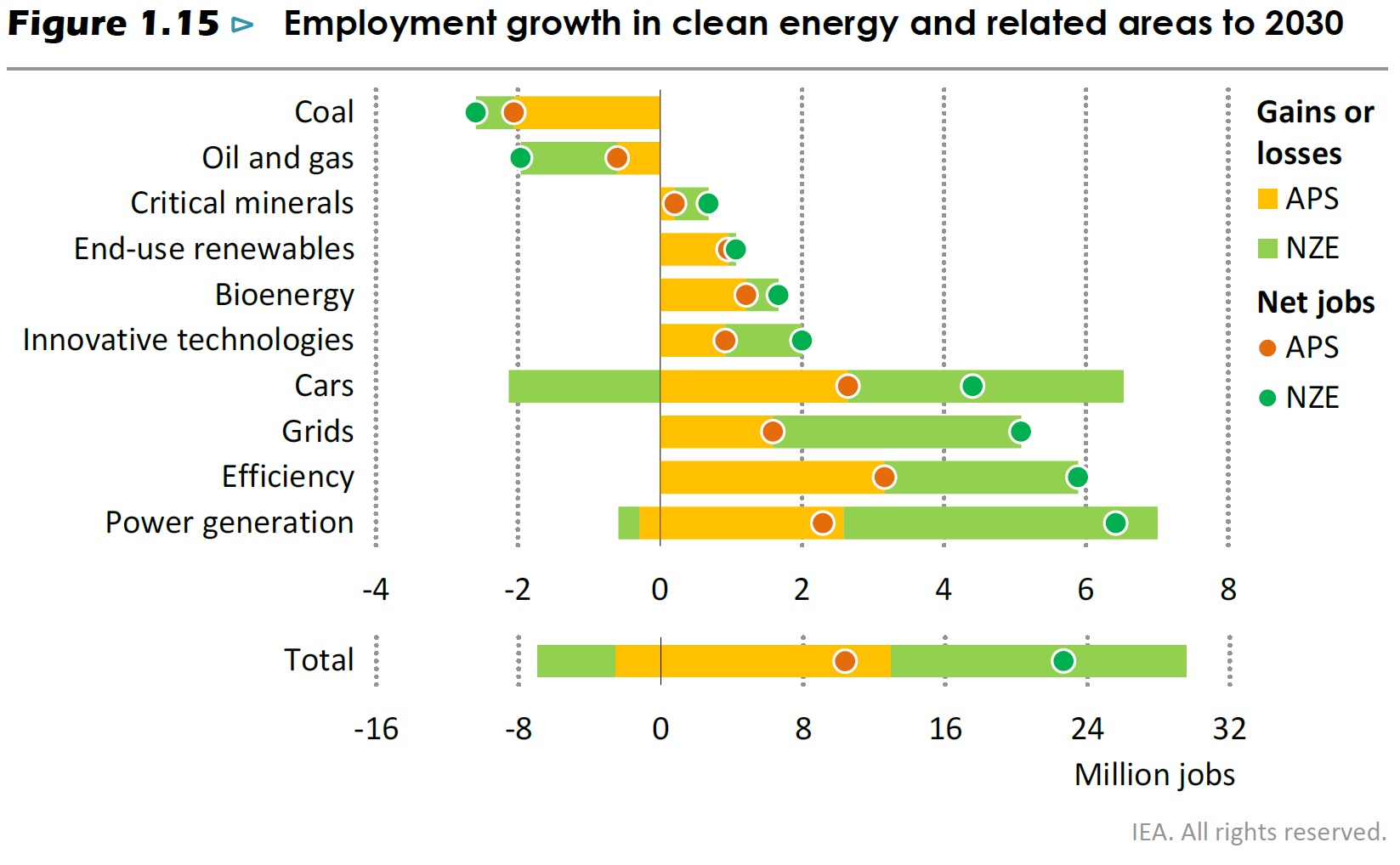

Employment in clean energy areas is set to become a very dynamic part of labour markets, with growth more than offsetting a decline in traditional fossil fuel supply sectors. As well as creating jobs in renewables and energy network industries, clean energy transitions increase employment in areas such as retrofits and other energy efficiency improvements in buildings, and the manufacturing of efficient appliances and electric and fuel cell vehicles. In total, an additional 13 million workers are employed in clean energy and related sectors by 2030 in the APS – and this figure doubles in the NZE.

Making the 2020s the decade of massive clean energy deployment will require unambiguous direction from COP26

This WEO-2021 provides stark warnings about the pathway that we are on, but also clearheaded analysis of the actions that can bring the world onto a path towards a 1,5°C future – with a strong affirmation of the benefits that this would yield.

Governments are in the driving seat: everyone from local communities to companies and investors needs to be on board, but no one has the same capacity as governments to direct the energy system towards a safer destination. The way ahead is difficult and narrow, especially if investment continues to fall short of what is required, but the core message from the WEO-2021 is nonetheless a hopeful one.

The analysis clearly outlines what more needs to be done over the crucial next decade: a laser-like focus on driving clean electrification, improving efficiency, reducing methane emissions, and turbocharging innovation – accompanied by strategies to unlock capital flows in support of clean energy transitions and ensure reliability and affordability. Many of the actions described are cost-effective, and the costs of the remainder are insignificant compared with the immense risks of inaction. Realising the agenda laid out in this report represents a huge opportunity to change the global energy system in a way that improves people’s lives and livelihoods.

A wave of investment in a sustainable future must be driven by an unmistakeable signal from Glasgow.

This is the executive summary of the report